‘Blockchain’ is the buzz word on the internet! There are thousands of write-ups, podcasts and blogs about how blockchain and cryptocurrencies are going to turn the world upside down.

But the question is how exactly is this new technological marvel relevant to people like us, who either run small or mid-size businesses or related to them?

Now if you think blockchain and cryptocurrencies especially bitcoins are somewhat similar, then you are not alone (seriously, there’s absolutely no need to go back to the stone age)! In fact, it is a common enough misconception. The truth is, cryptocurrencies such as bitcoins are a powered by and operated on blockchain technology.

Blockchain is basically a platform-like technology on which one can build applications that work like a decentralized ledger. Each peer in the blockchain system has access to this ledger at once. This virtual ledger is capable of recording and verifying transactions or contracts of any kind between two parties.

The uniqueness of blockchain technology is that the system verifies and finalizes each transaction after cross-checking the information with the rest of peers present in the system. Only and only if a minimum of 51% peers have the same information, the transaction is authenticated. Once the transaction is authenticated, it gets added as ‘block’ at the end of the ‘chain’ of transactions. As each new transaction gets added to the end of the chain, it becomes near impossible the alter any aspect of a transaction once verified. Cryptocurrencies, of which bitcoin is the most popular one right now, uses this technology to facilitate virtual (truly) peer to peer transactions that do not involve any third parties such as banks or currency exchanges.

In order to understand how small and mid-size businesses can use this ground-breaking technology, one must understand how it works!

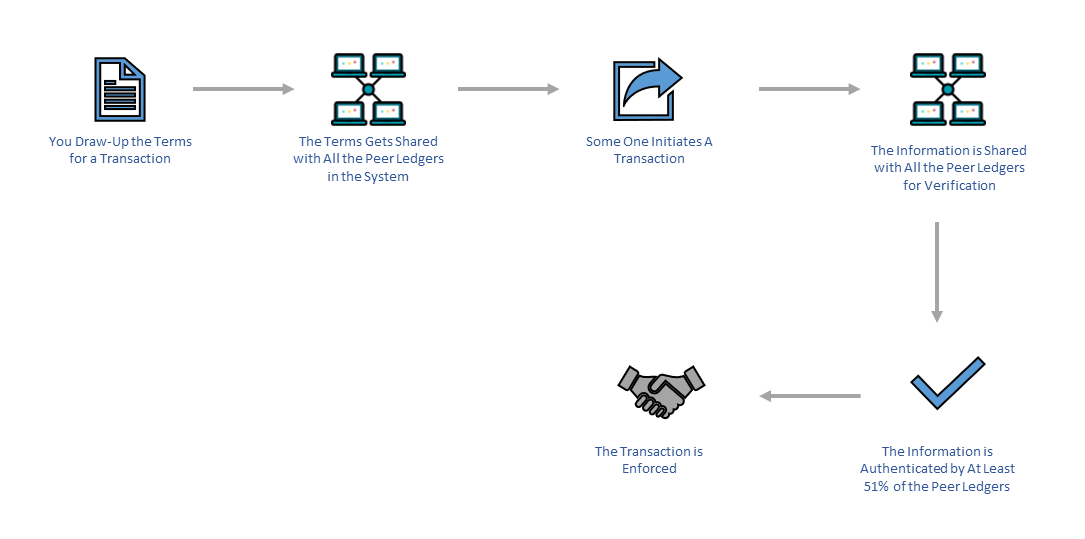

To put it simply, blockchain technology works in three steps, Create Transactions, Verify Transactions and Enforce Transactions.

Let me give you an example here!

Suppose, you are a writer who wants to sell advertising jingles for $100. Now, you draw up a blockchain contract with transaction terms such as ‘free to view, $100 to use commercially’. As soon as you create this transaction terms it gets stored in every ledger in the system. Now once a buyer comes and initiates purchase of the said jingles, the money will be held in escrow and the transaction will automatically be verified with each peer ledger in the system. If the information on your ledger matches at least 51% of the peer ledgers, the transaction will get verified and you’ll receive the money, even as the buyer receives the rights for the jingles.

So far, so good! But that still does not explain, why you as a small business owner should understand or learn about blockchain. Or how you can utilise this technology for your business.

Here’s how!

Smart Contracts: Most businesses have to deal with contracts of varied nature. Blockchain technology can be used to draft and enforce smart contracts about anything and everything between two parties.

What are smart contracts? A smart contract is nothing, but a protocol coded into a blockchain system that facilitates or enforces the performance any contract between two parties when the criteria are met and verified by at least 51% of the peers.

These smart contracts have enormous potential for small and mid-size businesses, as they completely do away with the need of any controlling third party such as insurance agencies or banks. The decentralized ledge and automated enforcement mean that everything from start-ups loans to real estate transaction can be done without incurring huge third-party fees and delays.

Monetary Exchange: Given the fact that Bitcoin is the most talked about blockchain application today, you already know this. As a small business, you can use cryptocurrencies to pay your vendors, suppliers, even your employees in a fast and secure manner.

One great advantage of cryptocurrency is that it is universal. In this age, when most businesses depend on overseas vendors and suppliers, have their team scattered around the globe and sell across borders, cryptocurrency can help you bypass currency exchanges and remove the burden of huge fees.

Blockchain is truly the technology of the future. And if one is to believe the experts, the future of commerce and economy is going to be heavily dependent on blockchain. While it may sound a bit too much right now, considering the following benefits, it is definitely not unlikely.

Yes, blockchain is still looked upon as a technology of the future. Yes, widespread use of this technology is still not there. But, depending on how versatile the technology is, there is no doubt that businesses around the world will catch up on it soon.

Be a little wiser and start implementing blockchain for your business! Better be the leader than a follower.